Complete guide to avail personal loan

Personal Loan Your Saviour During Those Tough Times in Life

How to apply personal loan online?

Ways to Generate Funds without taking a Personal Loan

Questions to ask Lenders before Committing to a Personal Loan

How to Get a Business Loan for Your Startup

5 Questions your Business Loan Lender May Ask When you Apply for a Business Loan

What you need to know about business loans before scaling up your business

5 Point Checklist for a Small Business Loan

Biggest Myths about of Small Business Loans

4 Things I Learnt After Taking An Education Loan

Must Know Facts about an Education Loan

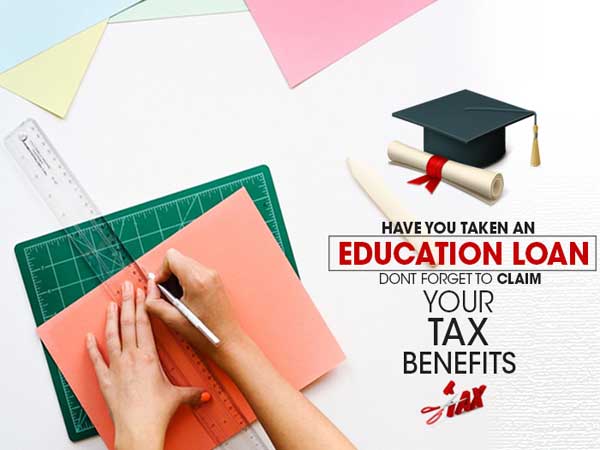

Tax benefits on education loan

How to Get out of Education Loan Debt Trap

Education Loan: 5 Sins You Must Avoid

Balance transfer of a loan happens when the entire unpaid principal loan amount is transferred to another bank for a lower rate of interest. This allows you to make effective, tactical use of existing interest rates that are being offered by different banks across the country. If you have paid your dues on time without defaulting, then this process is usually quite simple.

For example, if Bank A is offering a lower interest rate than your current bank for Balance Transfer, then you can transfer the remaining principle amount to Bank A and pay off the rest of the interest on the lower rate that Bank A is offering.

However, Balance Transfers might not always be lucrative. A cost-benefit analysis has to be done before you make your decision. There are three factors that have to be accounted for: